All Categories

Featured

Table of Contents

Which one you pick depends upon your requirements and whether the insurer will certainly approve it. Plans can also last until specified ages, which most of the times are 65. Due to the numerous terms it offers, level life insurance policy offers prospective policyholders with versatile alternatives. Beyond this surface-level info, having a better understanding of what these plans require will aid guarantee you acquire a policy that meets your needs.

Be conscious that the term you select will certainly affect the premiums you spend for the policy. A 10-year degree term life insurance plan will certainly cost much less than a 30-year plan because there's much less opportunity of an event while the plan is energetic. Reduced danger for the insurer corresponds to lower costs for the insurance holder.

Your household's age should likewise influence your plan term option. If you have kids, a longer term makes sense since it safeguards them for a longer time. If your youngsters are near the adult years and will be monetarily independent in the close to future, a shorter term might be a much better fit for you than an extensive one.

When comparing entire life insurance policy vs. term life insurance coverage, it deserves keeping in mind that the latter commonly sets you back less than the previous. The outcome is much more insurance coverage with lower premiums, offering the ideal of both worlds if you need a significant amount of insurance coverage but can not afford a more costly plan.

What is Term Life Insurance With Accelerated Death Benefit? Explained in Simple Terms?

A level death benefit for a term plan usually pays as a round figure. When that takes place, your successors will obtain the entire amount in a single settlement, which amount is ruled out earnings by the IRS. Those life insurance coverage earnings aren't taxable. Nevertheless, some level term life insurance policy companies permit fixed-period repayments.

Rate of interest payments got from life insurance policy plans are considered earnings and go through taxes. When your level term life plan ends, a couple of different things can happen. Some insurance coverage terminates instantly with no alternative for revival. In other situations, you can pay to prolong the strategy beyond its initial day or convert it right into a long-term plan.

The drawback is that your eco-friendly level term life insurance coverage will come with greater premiums after its preliminary expiry. Advertisements by Cash.

Life insurance policy companies have a formula for calculating risk utilizing mortality and passion (Level term life insurance definition). Insurers have thousands of clients securing term life plans simultaneously and utilize the costs from its active plans to pay making it through recipients of other plans. These business utilize death tables to estimate just how several individuals within a specific group will file fatality insurance claims per year, and that info is made use of to identify typical life span for prospective insurance policy holders

Furthermore, insurance provider can spend the money they get from costs and boost their earnings. Since a level term plan does not have cash worth, as an insurance holder, you can't spend these funds and they don't offer retired life income for you as they can with entire life insurance policy plans. Nevertheless, the insurance firm can spend the money and make returns.

The list below section details the advantages and disadvantages of level term life insurance policy. Foreseeable premiums and life insurance policy protection Simplified plan framework Prospective for conversion to permanent life insurance policy Limited insurance coverage duration No cash money value buildup Life insurance policy premiums can boost after the term You'll discover clear advantages when comparing level term life insurance coverage to other insurance policy kinds.

What is Term Life Insurance For Couples? How It Helps You Plan?

From the moment you take out a plan, your costs will never change, helping you plan economically. Your insurance coverage will not vary either, making these plans reliable for estate planning.

If you go this course, your premiums will raise yet it's always great to have some flexibility if you want to maintain an energetic life insurance coverage policy. Renewable level term life insurance policy is one more option worth considering. These plans permit you to keep your current plan after expiration, giving flexibility in the future.

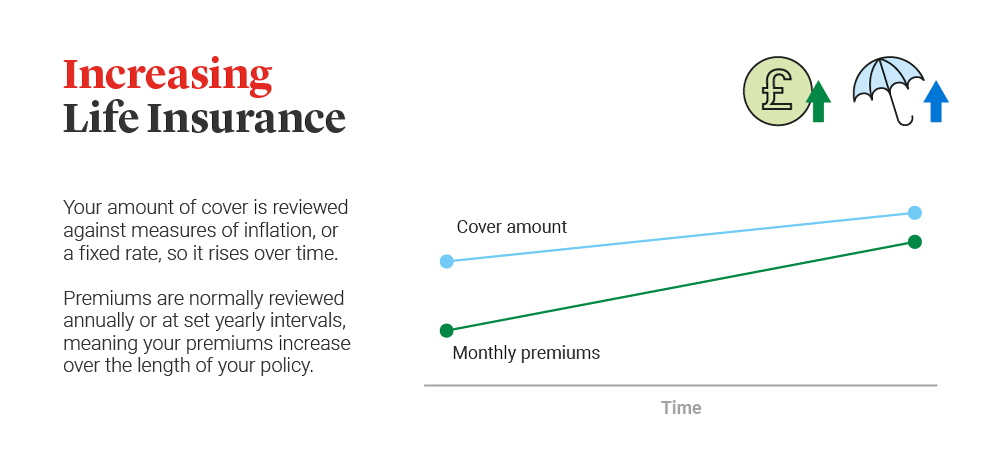

All About Increasing Term Life Insurance Coverage

Unlike a entire life insurance policy plan, level term protection does not last indefinitely. You'll pick a protection term with the most effective level term life insurance prices, yet you'll no more have insurance coverage once the plan runs out. This downside can leave you clambering to discover a new life insurance policy plan in your later years, or paying a costs to expand your current one.

Many entire, universal and variable life insurance policy plans have a money worth part. With one of those plans, the insurance company deposits a portion of your regular monthly costs settlements right into a cash money value account. This account gains interest or is invested, helping it grow and give an extra considerable payout for your recipients.

With a level term life insurance policy policy, this is not the situation as there is no cash worth element. As an outcome, your plan will not grow, and your survivor benefit will never enhance, thereby restricting the payout your beneficiaries will certainly receive. If you desire a plan that supplies a fatality advantage and develops money value, explore whole, global or variable strategies.

The 2nd your plan ends, you'll no longer live insurance policy protection. It's typically possible to renew your plan, but you'll likely see your costs raise substantially. This can present issues for retired people on a fixed revenue since it's an additional expenditure they might not have the ability to manage. Degree term and lowering life insurance policy deal comparable policies, with the main distinction being the fatality benefit.

It's a type of cover you have for a particular quantity of time, called term life insurance policy. If you were to die during the time you're covered for (the term), your liked ones obtain a fixed payout agreed when you obtain the policy. You simply select the term and the cover amount which you can base, for instance, on the expense of increasing youngsters up until they leave home and you could utilize the payment in the direction of: Aiding to pay off your mortgage, financial obligations, credit report cards or financings Assisting to spend for your funeral costs Aiding to pay university charges or wedding event prices for your youngsters Assisting to pay living prices, replacing your earnings.

How Does Level Term Vs Decreasing Term Life Insurance Policy Work?

The plan has no cash value so if your repayments quit, so does your cover. If you take out a degree term life insurance plan you might: Choose a repaired amount of 250,000 over a 25-year term.

{kind=link}

Latest Posts

Instant Quotes Life Insurance

Funeral Expense Benefits For Seniors

Funeral Insurance Underwriters