All Categories

Featured

Table of Contents

Level term life insurance policy is a policy that lasts a collection term normally in between 10 and three decades and features a degree fatality advantage and degree costs that stay the exact same for the entire time the plan is in impact. This indicates you'll understand exactly just how much your payments are and when you'll need to make them, allowing you to budget plan as necessary.

Level term can be a great alternative if you're aiming to get life insurance policy coverage for the very first time. According to LIMRA's 2023 Insurance Measure Research Study, 30% of all grownups in the United state demand life insurance coverage and don't have any type of type of plan. Level term life is foreseeable and economical, that makes it among one of the most prominent sorts of life insurance policy.

A 30-year-old male with a similar account can anticipate to pay $29 each month for the very same protection. AgeGender$250,000 insurance coverage amount$500,000 insurance coverage amount$1 million protection amount20Female$15$23$34Male$19$29$4830Female$15$23$37Male$18$29$4940Female$22$35$61Male$25$43$7550Female$44$78$139Male$57$102$18860Female$108$194$355Male$149$268$500 Collapse table Methodology: Typical monthly rates are calculated for male and women non-smokers in a Preferred health classification getting a 20-year $250,000, $500,000, or $1,000,000 term life insurance policy policy.

:max_bytes(150000):strip_icc()/Investopedia-terms-termlife-6451fde927474d4f8a81a5681efd393f.jpg)

Prices may vary by insurance provider, term, protection amount, health class, and state. Not all policies are offered in all states. It's the most inexpensive kind of life insurance coverage for most people.

It enables you to budget plan and prepare for the future. You can quickly factor your life insurance policy right into your spending plan since the costs never ever change. You can prepare for the future equally as easily since you know specifically just how much cash your loved ones will get in the event of your absence.

Is Level Term Life Insurance Policy a Good Option for You?

In these instances, you'll generally have to go with a brand-new application process to get a far better rate. If you still require protection by the time your degree term life policy nears the expiry day, you have a few choices.

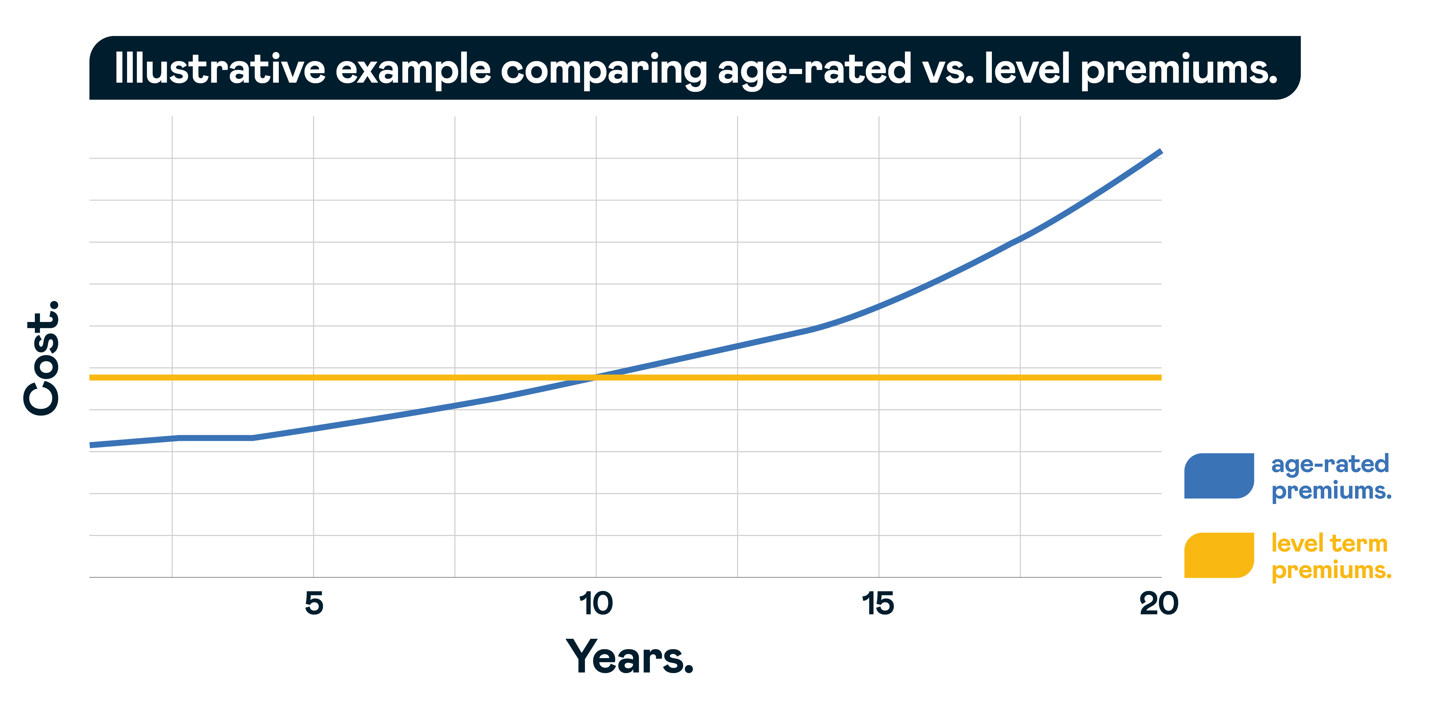

Most level term life insurance policy policies feature the option to renew insurance coverage on a yearly basis after the preliminary term ends. The expense of your plan will be based upon your existing age and it'll enhance annually. This can be a good alternative if you only need to expand your coverage for one or 2 years or else, it can get pricey quite rapidly.

Level term life insurance is among the most affordable protection choices on the marketplace due to the fact that it supplies basic defense in the kind of fatality benefit and just lasts for a collection time period. At the end of the term, it expires. Whole life insurance policy, on the various other hand, is considerably much more costly than level term life since it does not run out and features a cash worth attribute.

Not all plans are readily available in all states. Degree term is an excellent life insurance policy alternative for the majority of individuals, but depending on your insurance coverage requirements and personal situation, it might not be the best fit for you.

Annual renewable term life insurance policy has a regard to only one year and can be renewed each year. Annual renewable term life costs are at first less than level term life premiums, but prices rise each time you restore. This can be a good alternative if you, for instance, have simply quit smoking cigarettes and need to wait two or 3 years to apply for a degree term plan and be eligible for a reduced rate.

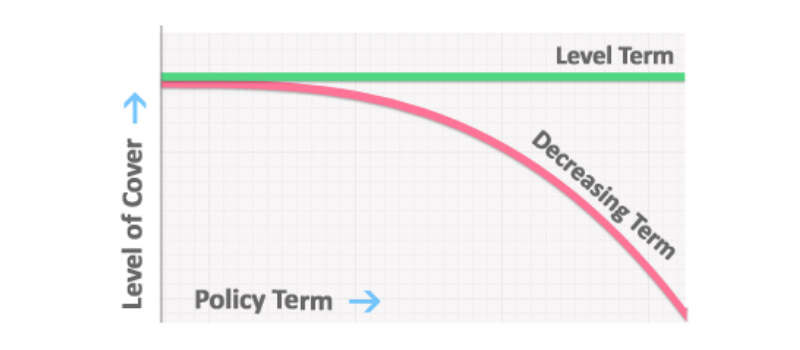

With a lowering term life policy, your death advantage payment will reduce over time, yet your repayments will certainly remain the exact same. Decreasing term life policies like mortgage defense insurance coverage normally pay out to your lender, so if you're looking for a plan that will pay to your loved ones, this is not an excellent suitable for you.

What Exactly Is Guaranteed Level Term Life Insurance Coverage?

Increasing term life insurance policy policies can assist you hedge versus inflation or plan economically for future youngsters. On the various other hand, you'll pay more ahead of time for less protection with a raising term life plan than with a level term life policy. 20-year level term life insurance. If you're not exactly sure which sort of policy is best for you, working with an independent broker can help.

Once you've decided that level term is appropriate for you, the following step is to buy your plan. Below's exactly how to do it. Determine just how much life insurance policy you need Your insurance coverage quantity need to supply for your family's lasting economic demands, consisting of the loss of your revenue in the event of your fatality, along with financial obligations and daily costs.

The most preferred type is currently 20-year term. Most business will certainly not market term insurance coverage to a candidate for a term that ends previous his or her 80th birthday celebration. If a plan is "renewable," that means it continues effective for an added term or terms, approximately a specified age, also if the wellness of the guaranteed (or other factors) would certainly trigger him or her to be declined if she or he obtained a new life insurance policy.

So, premiums for 5-year renewable term can be degree for 5 years, after that to a new rate reflecting the new age of the guaranteed, and so on every 5 years. Some longer term plans will certainly assure that the premium will certainly not raise during the term; others do not make that guarantee, making it possible for the insurance provider to increase the rate throughout the policy's term.

Discover What Term Life Insurance For Seniors Is

This means that the policy's owner deserves to alter it right into a permanent kind of life insurance policy without added evidence of insurability. In many sorts of term insurance policy, including homeowners and car insurance coverage, if you have not had a claim under the plan by the time it expires, you get no reimbursement of the costs.

Some term life insurance policy customers have actually been miserable at this result, so some insurance companies have produced term life with a "return of costs" function. The costs for the insurance with this function are typically significantly higher than for policies without it, and they normally require that you keep the policy in force to its term or else you forfeit the return of premium benefit.

Level term life insurance policy premiums and survivor benefit continue to be constant throughout the policy term. Level term plans can last for periods such as 10, 15, 20 or 30 years. Degree term life insurance policy is commonly more economical as it doesn't construct money worth. Level term life insurance is one of the most typical kinds of security.

While the names often are made use of mutually, degree term coverage has some crucial distinctions: the premium and death advantage stay the very same for the duration of coverage. Degree term is a life insurance plan where the life insurance coverage costs and survivor benefit stay the same throughout of protection.

{kind=link}

Latest Posts

Instant Quotes Life Insurance

Funeral Expense Benefits For Seniors

Funeral Insurance Underwriters